Never has there been a one size fits all solution for resolving debt-related disputes, especially in China, as market shakeups bring increasingly complex issues. Sophie Cheng reports

In 2025, China saw the long-awaited revival of its capital markets, with the Shanghai Composite Index reaching a 10-year high. Alongside this surge came equity investment exits and related disputes.

Faced with the pressing needs for debt recovery, companies are weighing litigation, enforcement and bankruptcy liquidation with greater caution, exploring new strategies.

With the revised Company Law in force for more than a year, businesses are caught between old norms and new, realising an unprecedented demand for strategic agility. Meanwhile, technological innovation continues to introduce novel forms of challenges and solutions to disputes.

Move with the capital

Observing the strong capital market momentum, Deng Youping, a Beijing-based partner at Jingtian & Gongcheng, says opportunities are arising for investors to achieve their primary goal of exiting through listings. This is often done by extending the timetable for IPOs or performance-linked bet-on agreements – also known as valuation adjustment mechanism agreements – that tie investor returns to company performance targets.

Zhang Yiwen, a partner at Llinks Law Offices in Shanghai, also notes a growing trend among investors to back portfolio companies in seeking listing opportunities. This has made negotiations and settlements, both within and outside formal dispute resolution, more commonplace between investors and counterparties, subject to share repurchase obligations.

Such negotiations may themselves give rise to new disputes. Zhang says some investors, particularly those backed by state-owned assets, often use deferrals on repurchase obligations as leverage to seek compensation from companies and their controlling shareholders. These side arrangements are typically negotiated privately between individual investors and controllers, and are signed in so-called “drawer agreements”, meaning contracts kept off the official books.

Such “drawer agreements” pose challenges to regulatory order in primary and secondary markets, and often trigger disputes over enforceability. Zhang explains: “For investors in the primary market, when a company grants financial compensation to selective investors in exchange for deferring repurchase obligations, it clearly amounts to unequal treatment of other investors. As a result, investors today are increasingly cautious towards such practices in negotiations, with mutual suspicion steadily deepening.”

Zhang adds that these hidden agreements may violate regulatory requirements mandating disclosure and clearance of special arrangements between investors and controlling shareholders at the time of listing.

“At present, there is no clear and consistent judicial standard on whether drawer agreements that breach disclosure and cleanup rules should be deemed valid,” he says. “Consequently, many investors, when drafting compensation or make-up clauses with companies, repeatedly revise the wording and calculation methods in light of recent cases, attempting to reduce the risk of invalidity.”

With markets gaining strength, Yan Hao, a partner at Tian Yuan Law Firm in Beijing, advises that special attention should be paid to the validity of “bottom-line commitments” – agreements in which controlling shareholders personally guarantee returns for pre-IPO investors.

In June 2022, the Supreme People’s Court issued its Opinions on Providing Judicial Safeguards for the Deepening of the NEEQ Reform and the Establishment of the Beijing Stock Exchange, article 9 of which held that guarantee agreements signed between investors and controlling shareholders in the course of IPO financing or post-IPO private placements are invalid.

“Although this judicial interpretation was directed at companies listed on the NEEQ and the Beijing Stock Exchange, some court rulings in recent years have begun to extend its application to listed companies beyond these venues,” says Yan.

Zhou Zheren, a managing partner at the Shanghai office of Grandall Law Firm, observes views on the limitation period for exercising share repurchase rights. He points out that China’s official judicial Q&A platform selected response issued in August last year (batch IX), along with more recent judicial rulings, established a six-month exercise period. Exercising repurchase rights within this period signals the commencement of the limitation period for initiating legal action. Failure to do so means the lapse of such rights.

An opposite view was expressed in two articles published this year by the Supreme People’s Court in its journal, Application of Law. “This reflects the ongoing uncertainty over the limitation period for exercising repurchase rights in judicial practice,” says Zhou.

In arbitration, Zhou says that tribunals generally take a more pragmatic view, evaluating cases involving equity repurchases through commercial practice, parties’ reasonable expectations, and autonomy of will. He advises rights holders to secure as long an exercise window as possible, specify it in the agreement, and set strict deadlines for the obligor’s performance and penalties for breach.

Once repurchase conditions are met, the rights holder should promptly notify obligors within the agreed, or a reasonable, period, stating the timeframe and manner of performance. Continual reminders are also essential, adds Zhou, to avoid the claim being barred by time limitations.

In securities misrepresentations, particularly stock-related ones, Zhang, of Llinks, sees progress in how courts assess materiality. Courts now adopt more standardised criteria by weighing listed companies’ disclosures, trading volumes, price movements, and the proportion of misrepresentation relative to financial indicators.

“The analysis is becoming more sophisticated – for example, courts now look at whether there was overreaction in the securities market, and which industry indices should serve as the benchmark for price comparisons,” he says. “It is foreseeable that the stock-related misrepresentation cases will increasingly be handled through modular and factor-based frameworks.”

Zhou Wei, an equity partner at Zhong Lun Law Firm in Beijing, also notes that courts are more focused on examining transaction causation. Factors such as the “proximate cause”, which, unlike actual cause, refers to the primary reason as recognised by law, and the impact of other significant events are now part of causation analysis.

At the same time, the evaluation and quantification of systemic and non-systemic risks on investor losses has gained acceptance in judicial practice, with third-party institutions routinely engaged to determine damages.

“As for the liability of directors, supervisors, senior executives and intermediaries, there is a growing consensus in practice that proportional joint liability should be allocated based on the degree of fault and causal contribution of each responsible party,” she says.

Paths to recovery

Evolving legislative and judicial developments are offering businesses fresh insights into litigation strategies for debt recovery. “Enterprises should structure their strategies around two pillars: people and assets,” says Deng, at Jingtian & Gongcheng.

On the “people” side, Deng explains that, before filing suit, companies should review whether guarantees or debt assumption arrangements exist to determine whether parties beyond the debtor should be named as co-defendants. In enforcement proceedings, he suggests applying to courts to add or substitute liable parties as judgment debtors and impose measures such as consumption restrictions or inclusion on the judgment defaulters’ list to encourage repayment.

On the “assets” side, Cao Lijun, a Beijing-based equity partner at Zhong Lun, urges timely property preservation both before and after litigation. This includes freezing the debtor’s or related parties’ assets – especially bank deposits, equity interests and real estate – to prevent asset transfers that could render enforcement ineffective.

When a debtor is insolvent and its assets are already frozen by multiple courts, leading to a race among creditors, Li Zhao, a partner at the Beijing head office of Commerce & Finance Law Offices, describes initiating bankruptcy proceedings as “one of the most effective ways to break the deadlock and maximise debt recovery”.

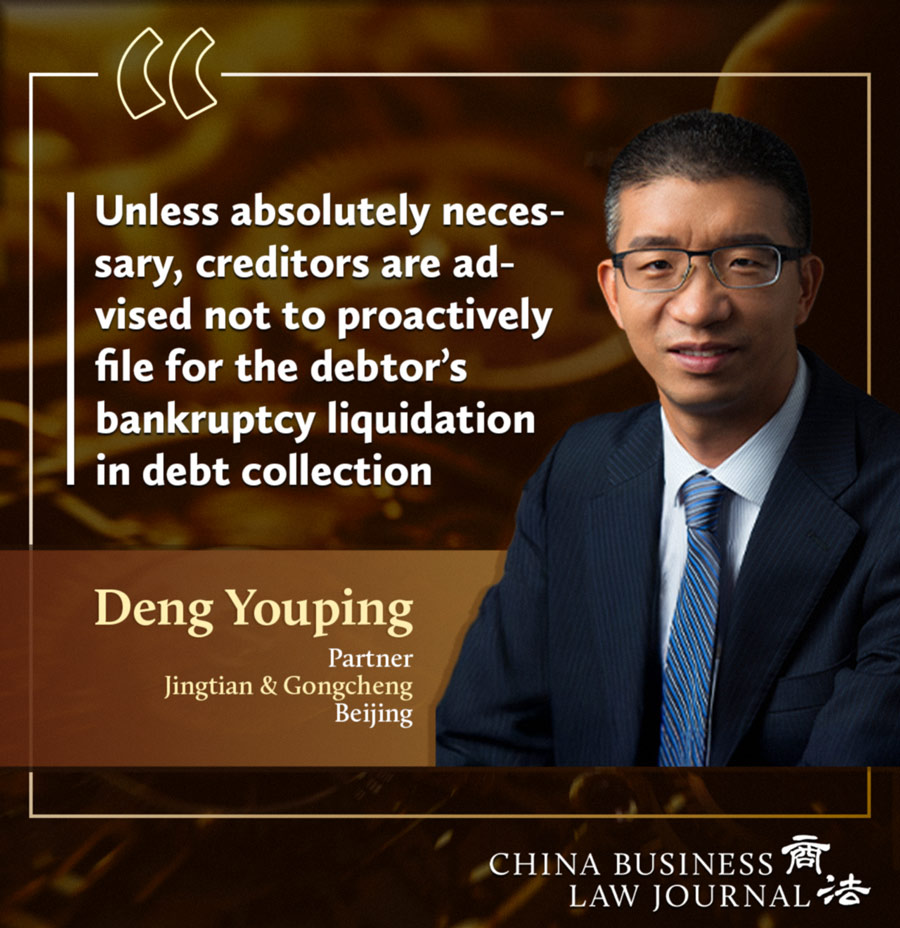

However, Deng cautions that “unless absolutely necessary, creditors are advised not to proactively file for the debtor’s bankruptcy liquidation in debt collection”. He says that liquidation may deprive the debtor of survival opportunities, and creditors then typically recover as little as 15% to 30% of their claims.

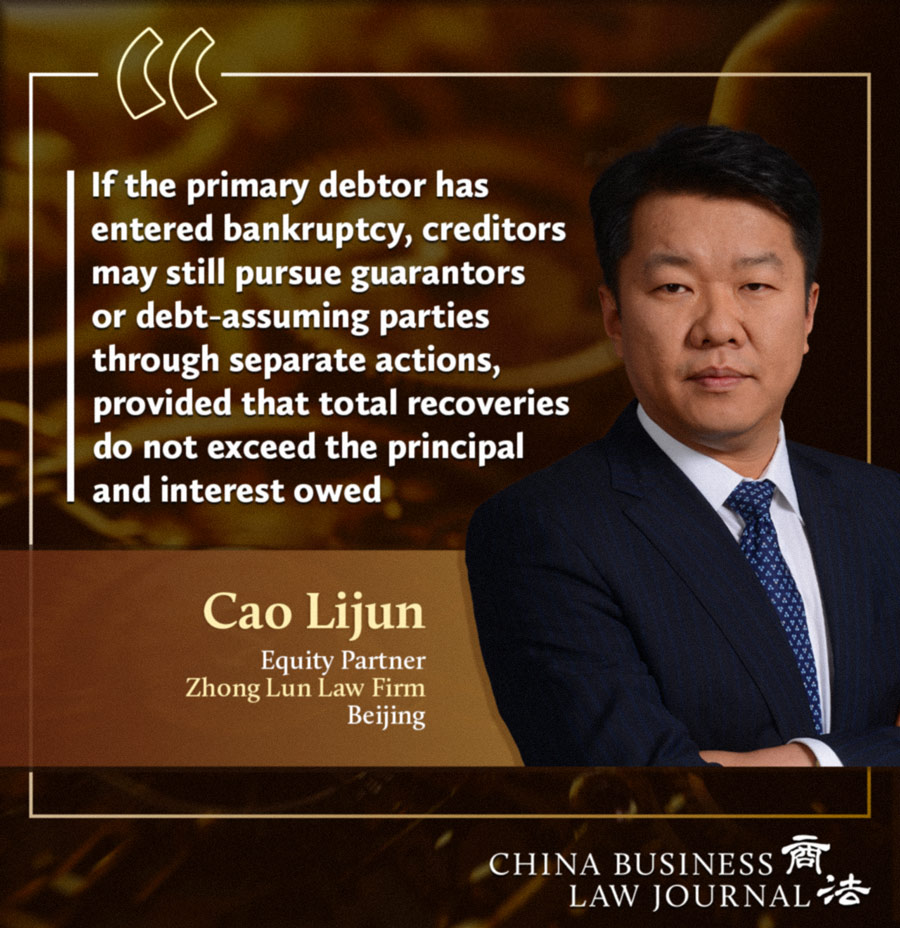

Cao stresses that bankruptcy should be used only when the debtor is clearly insolvent and no other liable parties exist. “If the primary debtor has entered bankruptcy, creditors may still pursue guarantors or debt-assuming parties through separate actions, provided that total recoveries do not exceed the principal and interest owed,” he says.

To address enforcement difficulties, Li recommends investigating “hidden assets” by tracing upstream and downstream enterprises, public bidding information and financial statements to identify any collectible receivables. If a debtor neglects to exercise its claims or rights in a way that impairs creditors’ recovery, creditors may bring a subrogation action against the secondary debtor.

Regarding the creditors’ right of revocation, although the Judicial Interpretation on the General Principles of Contract Law provides more detailed guidance, Zhang cautions that “these provisions do not allow creditors to immediately recover dispersed assets from secondary debtors in a single step. Courts differ on whether the creditors’ subrogation and revocation rights can be fully integrated.”

Deng suggests using special legal provisions to initiate new actions against parties related to the debtor. He says that if a shareholder of a corporate debtor has failed to perform capital contribution obligations, it may be appropriate to assess whether conditions such as accelerated maturity of contributions are met, and then sue the shareholder for supplementary compensation to the extent of the outstanding contributions.

Many enforcement issues involve adding shareholders with defective contributions, which remains controversial in judicial practice, according to Zhang. “Given that the prevailing judicial view treats amounts recovered from shareholders in separate actions as direct repayment rather than funds entering company accounts, creditors can still safeguard their interests by separately suing shareholders for damages caused to the company’s creditors,” he says.

Re-learn the rules

More than a year has passed since the amended Company Law came into effect. Summarising his case-handling experience, Zhang says the most profound impact on enterprises lies in the new rules on corporate capital regimes. These include accelerated capital contribution deadlines, shareholder liability for transfers of both matured and unmatured equity contributions, unlawful profit distributions, illegal capital reductions, and false statements made during simplified deregistration.

“The implementation of the new law is essentially a transition and collision between old and new regulatory regimes,” says Zhou Zheren, of Grandall. “As market participants, companies must respect the updated framework, adjust their governance structures, and respond proactively to the challenges of legal reform through systemic compliance reviews, stronger internal supervision, and risk alert mechanisms.”

Zhou recommends: reviewing articles of association to ensure shareholder rights, obligations and governance procedures align with the amended Company Law; optimising powers between the board of directors and supervisory board; establishing compliance management departments; strengthening financial independence and internal control systems; verifying the authenticity of capital contributions; defining control rights to prevent capital withdrawal and financial commingling; preparing contingency plans for shareholder derivative lawsuits; adopting pre-approval compliance mechanisms; and expanding directors’ and officers’ liability insurance.

Technological innovation is also reshaping the equity investment market, with industries such as AI and virtual assets drawing attention, but the integration of new technologies has created as many challenges as conveniences.

Zhong Lun’s Cao points out that liability allocation for algorithm-driven decision making, the legal characterisation of virtual assets, and the compliance of related transactions remain subject to inconsistent judicial standards. New forms of evidence, including electronic data trails and blockchain transaction records, also pose difficulties due to underdeveloped collection, preservation and court acceptance mechanisms.

“Enterprises should adhere to the principles of prioritising compliance and proactive risk management,” says Cao. “Specifically, they can collaborate with tech, legal or ethical experts to systematically build a risk prevention framework suited to emerging industries, while closely monitoring changes in domestic and international regulatory policies on cross-border data flow, so as to be fully prepared.”

Arbitration v litigation in commercial dispute resolution

By Wang Baohua, W&H Law Firm

Throughout the entire life cycle of a commercial transaction, the design and selection of a dispute resolution mechanism has become a critical component of a company’s risk management framework…

When civil meets criminal: Resolving finance conflicts

By Liu Jun, Kangda Law Firm

The Summary of the National Courts’ Symposium on the Trial Work of Financial Crime Cases states: “Cracking down on all types of financial crimes in accordance with the law is a long-term and important task for the people’s courts in criminal adjudication.”

Navigating administrative legal risks and dispute resolution

By Edwin Cao, Yong Sun Law Offices

With the deepening of reforms to streamline administration, strengthen regulation and upgrade services – all aimed at optimising the business environment – regulatory touchpoints are now deeply embedded in business operations…

Risk boundaries of dual controllers under Company Law

By Liu Jing and Gao Xiya, Han Kun Law Offices

In corporate governance, power often extends beyond the votes cast at the boardroom table. In practice, certain individuals, although holding no formal position within the company,

Shielding financial investors from M&A fraud liability

By Li Fangzhe and Liang Qiang, Zhongce

In recent M&A cases, financial investors have increasingly faced civil liability or criminal prosecution due to fraud committed by target companies…

2025")